AI personal finance automation is the most consistently skipped infrastructure investment among the builders most capable of implementing it — and the irony is concrete: the same person who writes automated cash sweep code for a client’s treasury stack often tracks their own expenses in a spreadsheet they update twice a month if they remember.

The data behind this gap is specific. Origin’s analysis of 12,000 household accounts found that 68% of consumers couldn’t predict their month-end balance within $200. That’s not a financial literacy problem. That’s a tool problem — the same kind of tool problem that structured agentic systems solve in every other domain builders work in. AI personal finance automation deployed correctly closes this gap: 50% better forecast accuracy, 5 or more hours saved monthly on financial management, and hidden subscription waste discovered automatically rather than discovered on credit card statements three months late.

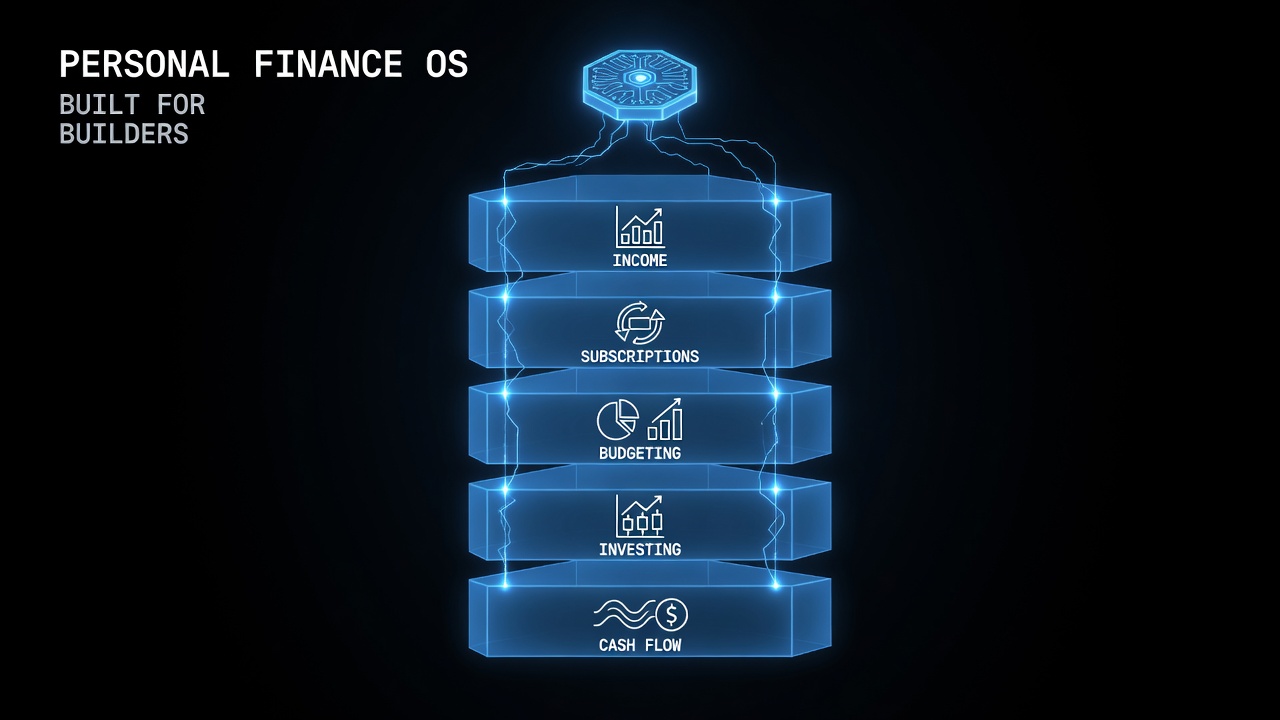

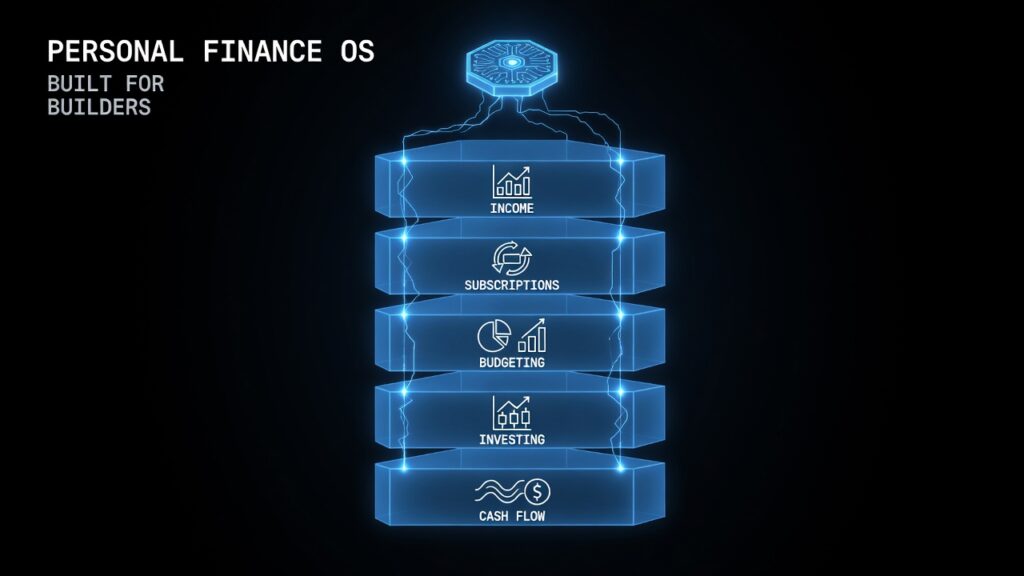

This post gives you the builder-specific personal finance OS — five layers stacked in sequence — and the anomaly detection code that catches the subscription creep and cash flow surprises that manual tracking consistently misses.

Why Builders Need AI Personal Finance Automation More Than Most

The standard personal finance advice is built around a salaried employee with predictable monthly income. Builders running agentic operations, consulting practices, or product businesses have a structurally different financial profile that standard advice handles poorly:

- Irregular income. A month where three client invoices clear simultaneously followed by a month where none do creates a cash flow variance that a static budget can’t absorb. Manual management of that variance requires constant attention; AI personal finance automation handles it with real-time buffer logic.

- High SaaS subscription overhead. A builder’s monthly tooling stack — AI API credits, Claude Max, development environments, deployment infrastructure, analytics tools, design tools — commonly runs $300 to $800 per month before any project-specific spend. The average person doesn’t know 30% of their subscriptions exist; the average builder doesn’t know 40% of their subscriptions are still active from projects that ended.

- Self-employment tax complexity. Quarterly estimated payments, deductible business expenses, and the self-employment tax rate create a financial management overhead that employees never deal with. AI personal finance automation that separates business and personal spend automatically and flags tax-relevant transactions is not optional infrastructure for a solo operator — it’s what prevents the annual tax bill surprise.

The Solo Builder Burnout post in this series identified financial stress as one of the most consistent burnout contributors for independent operators. AI personal finance automation is the structural fix — not because it solves every financial problem, but because it removes the cognitive overhead of manual tracking from a workday that already has too many attention demands.

The Builder Personal Finance OS: Five Layers

Layer 1 — Income Splitting (Automated at Receipt)

The moment any payment clears, automated rules split it across four buckets: operating expenses (30%), taxes (25-30% depending on jurisdiction and income level), savings (15%), and deployable income (the remainder). Direct deposit splitting handles salaried income automatically on most bank platforms. For invoice income, a webhook from your invoicing platform can trigger the split the moment payment clears — the same webhook pattern from the Automated Invoicing Code post, applied to the receiving end of the payment rather than the sending end.

Layer 2 — Subscription Audit (Monthly Automated Scan)

The average subscription audit finds $50 to $150 in monthly charges the account holder either forgot about or could consolidate. For builders, this number is typically higher. A monthly automated scan that categorizes all recurring charges, flags any that haven’t generated an associated login or usage event in 30 days, and surfaces them for a single monthly review takes five minutes of attention instead of a recurring manual tracking task.

Layer 3 — Real-Time Budgeting (AI Categorization + Anomaly Detection)

Modern AI budgeting tools achieve 90 to 95% automatic transaction categorization accuracy, with the remaining exceptions surfaced for quick review rather than requiring manual classification of every transaction. The value add over traditional budgeting apps is anomaly detection: identifying spending patterns that deviate from your personal baseline — not just “you spent more than last month” but “you spent $340 more on infrastructure in the last two weeks, which is 2.8 standard deviations above your trailing 90-day average.” The second framing is actionable; the first is just a number.

Layer 4 — Automated Investing (Robo-Advisor + Tax Optimization)

A robo-advisor that receives automatic transfers on a fixed schedule, rebalances when allocations drift beyond a set threshold, and harvests tax losses automatically handles the investing layer with near-zero ongoing attention. For builders with irregular income, the transfer amount can be a fixed percentage of the previous month’s deployable income rather than a fixed dollar amount — maintaining the saving habit through low-income months without creating overdraft risk.

Layer 5 — Cash Flow Prediction (30-Day Rolling Forecast)

The layer that closes the 68% month-end-balance-uncertainty gap is a rolling 30-day cash flow forecast that incorporates known outflows (rent, subscriptions, estimated taxes, recurring invoices), probable inflows (expected invoice payments based on historical collection timing), and a buffer margin that accounts for irregular expenses. At 50% better forecast accuracy than manual tracking, AI personal finance automation at this layer eliminates the “I didn’t realize the quarterly tax payment was this week” incidents that cause unnecessary stress and occasionally unnecessary bank fees.

The Subscription Anomaly Detection Loop

The highest-ROI single implementation in the builder personal finance OS is the subscription audit loop — the one place where the average builder recovers real money within the first 30 days of running it. This connects directly to the AI Agent Revenue Loop post’s four-stage architecture: trigger, process, output, audit.

import os

import json

import anthropic

from datetime import datetime, timedelta

from decimal import Decimal

from dotenv import load_dotenv

load_dotenv()

client = anthropic.Anthropic(api_key=os.environ.get("ANTHROPIC_API_KEY"))

def load_transactions(days_back: int = 90) -> list[dict]:

"""

In production, replace this with a real bank API call —

Plaid, Teller, or your bank's direct API.

These are mocked transactions for illustration.

"""

today = datetime.now()

return [

{"date": (today - timedelta(days=2)).strftime("%Y-%m-%d"),

"description": "CLAUDE AI SUBSCRIPTION", "amount": -20.00},

{"date": (today - timedelta(days=30)).strftime("%Y-%m-%d"),

"description": "CLAUDE AI SUBSCRIPTION", "amount": -20.00},

{"date": (today - timedelta(days=7)).strftime("%Y-%m-%d"),

"description": "FIGMA SUBSCRIPTION", "amount": -15.00},

{"date": (today - timedelta(days=37)).strftime("%Y-%m-%d"),

"description": "FIGMA SUBSCRIPTION", "amount": -15.00},

{"date": (today - timedelta(days=14)).strftime("%Y-%m-%d"),

"description": "NOTION PRO ANNUAL", "amount": -96.00},

{"date": (today - timedelta(days=45)).strftime("%Y-%m-%d"),

"description": "DATADOG MONITORING", "amount": -189.00},

{"date": (today - timedelta(days=75)).strftime("%Y-%m-%d"),

"description": "DATADOG MONITORING", "amount": -189.00},

{"date": (today - timedelta(days=22)).strftime("%Y-%m-%d"),

"description": "GRAMMARLY PREMIUM", "amount": -12.00},

{"date": (today - timedelta(days=52)).strftime("%Y-%m-%d"),

"description": "GRAMMARLY PREMIUM", "amount": -12.00},

{"date": (today - timedelta(days=82)).strftime("%Y-%m-%d"),

"description": "GRAMMARLY PREMIUM", "amount": -12.00},

]

def detect_recurring_charges(transactions: list[dict]) -> list[dict]:

"""

Groups transactions by description and identifies recurring charges

with their frequency and total 90-day cost.

"""

groups: dict[str, list] = {}

for tx in transactions:

key = tx["description"].upper()

groups.setdefault(key, []).append(tx)

recurring = []

for desc, txs in groups.items():

if len(txs) >= 2:

amounts = [abs(t["amount"]) for t in txs]

monthly_cost = sum(amounts) / 3 # normalized to monthly

recurring.append({

"name": desc,

"occurrences_in_90_days": len(txs),

"avg_charge": sum(amounts) / len(amounts),

"estimated_monthly_cost": round(monthly_cost, 2),

"last_charge": max(t["date"] for t in txs)

})

return sorted(recurring, key=lambda x: x["estimated_monthly_cost"], reverse=True)

def ai_audit_subscriptions(recurring: list[dict]) -> dict:

"""

Uses Claude to analyze recurring charges and identify candidates

for cancellation, consolidation, or renegotiation.

"""

response = client.messages.create(

model="claude-sonnet-5",

max_tokens=800,

messages=[{

"role": "user",

"content": f"""You are a personal finance assistant for a solo software builder.

Review these recurring charges from the last 90 days and identify:

1. Any that appear to be unused or underused (based on name alone)

2. Any that could potentially be consolidated

3. The estimated annual savings if the top 3 candidates were cancelled

Recurring charges:

{json.dumps(recurring, indent=2)}

Respond in JSON with:

{{

"cancellation_candidates": [

{{"name": "...", "monthly_cost": N, "reason": "..."}}

],

"consolidation_opportunities": [

{{"names": ["...", "..."], "rationale": "..."}}

],

"estimated_annual_savings": N,

"action_priority": "immediate|review|keep"

}}"""

}]

)

try:

return json.loads(response.content[0].text)

except json.JSONDecodeError:

return {"raw_analysis": response.content[0].text}

def run_subscription_audit() -> dict:

"""

The full subscription audit loop: trigger → process → output → audit.

"""

print(f"\n[AUDIT START] {datetime.now().strftime('%Y-%m-%d %H:%M')}")

transactions = load_transactions(days_back=90)

recurring = detect_recurring_charges(transactions)

analysis = ai_audit_subscriptions(recurring)

monthly_total = sum(s["estimated_monthly_cost"] for s in recurring)

annual_projection = monthly_total * 12

result = {

"audit_date": datetime.now().isoformat(),

"subscriptions_found": len(recurring),

"monthly_total_usd": round(monthly_total, 2),

"annual_projection_usd": round(annual_projection, 2),

"ai_analysis": analysis,

"recurring_charges": recurring

}

print(f"[FOUND] {len(recurring)} recurring charges")

print(f"[TOTAL] ${monthly_total:.2f}/month (${annual_projection:.2f}/year)")

if isinstance(analysis, dict) and "estimated_annual_savings" in analysis:

savings = analysis["estimated_annual_savings"]

print(f"[OPPORTUNITY] ${savings:.2f} potential annual savings identified")

return result

if __name__ == "__main__":

result = run_subscription_audit()

print("\n[CANCELLATION CANDIDATES]")

ai = result.get("ai_analysis", {})

for candidate in ai.get("cancellation_candidates", []):

print(f" → {candidate['name']}: ${candidate['monthly_cost']}/mo — "

f"{candidate['reason']}")Run this against your actual bank transaction feed — via Plaid, Teller, or your bank’s direct API where available — and the audit typically surfaces $50 to $200 in monthly charges worth reviewing within the first run. At the builder’s tooling overhead level, the number is often higher.

The One Number That Changes How You Manage Cash Flow

The single most impactful output of AI personal finance automation for a builder with irregular income isn’t a dashboard — it’s one number updated daily: Days of Runway. Current liquid balance divided by average daily burn rate, updated each morning when transactions clear.

When that number sits comfortably above 90, the financial background noise that drains attention from architectural work disappears. When it drops below 60, it’s a visible signal to review the invoice pipeline and the cash sweep architecture — the same governed autonomy pattern from the Automated Cash Sweep post, now pointed at personal rather than business treasury.

For the full comparison of AI personal finance tools available in 2026, see Due’s personal finance automation guide.

The Builder’s Takeaway

AI personal finance automation is the application of the same architectural discipline this series applies to production pipelines, pointed at the financial system that funds the person running them. The five-layer OS — income splitting, subscription audit, real-time budgeting, automated investing, cash flow prediction — requires about four hours to set up and returns those hours within the first month. The subscription audit alone typically produces positive ROI within 30 days. The builder who has automated their client’s cash management but is still manually updating a budget spreadsheet is running a gap between their professional and personal infrastructure that has a concrete cost in time, attention, and occasional financial stress. The code above closes the first gap. The rest is configuration.

This post is part of The Agentic Protocol’s Wealth series — the autonomous capital layer beneath every agent pipeline. See also: AI Agent Unit Economics.